John Williams lives in a one-bedroom Oakland apartment just a few blocks behind the Grand Lake Theater. He doesn’t like to talk about politics, and he certainly doesn’t like to talk about the stock market. He’s sixty years old and has a two-man operation: a webmaster and himself. But in the obscure corners of the Internet, he’s an unlikely legend, an economist who publishes a newsletter that purports to tell the real truth about the state of the nation’s health. His thesis is both simple and surprisingly complex: over the course of thirty years, Washington politicians have pressured federal economists to tweak the methods by which they assess key metrics of the economy, to inflate the numbers and protect the incumbents from voters who would surely rise up in anger, if only they knew the truth.

And the truth, Williams claims, is that the economy has always performed much more poorly than the federal numbers indicate. Prices are higher, fewer people are working, and the economy is growing at a much slower pace. Even now, when the nation faces its greatest crisis since the Great Depression, the real dimensions of the disaster are still being obscured by gimmicks. It’s a message that has earned him an odd bit of notoriety, to the clear frustration of some of the country’s most prominent economists, who claim that Williams has built a career misrepresenting complex mathematical models and spreading panic.

Credits: Chris Duffey

Credits: Courtesy of ShadowStats.com

Credits: Courtesy of ShadowStats.com

Credits: Courtesy of ShadowStats.com

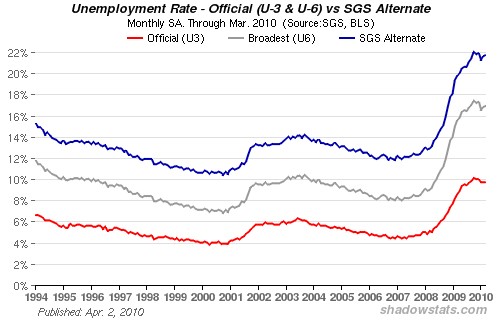

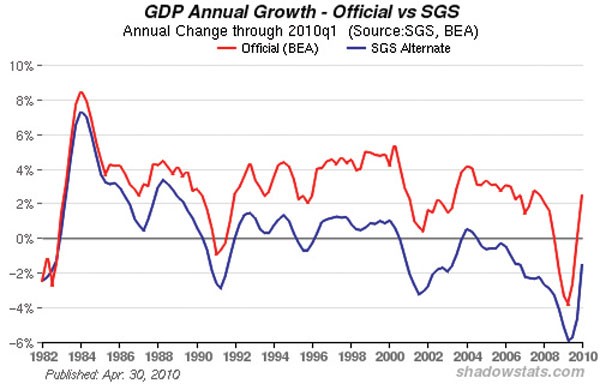

Take February, for example. What does Williams think was the true state of the economy? The official unemployment rate was listed at 9.7 percent, but according to Williams’ models, the real number, including part-time employees and workers who have just given up in despair, is closer to a staggering 21.6 percent. The official February inflation rate was 2.1 percent; Williams argues that it’s really around 5.5 percent. And GDP for the fourth quarter of 2009 was not 5.9 percent, as the government claims, but 2.9 percent.

Williams says he’s just using math to tell you what you already know — that your economic life, and that of your friends, is much worse than the government’s numbers say. Everywhere you go, you can feel it. The NUMMI plant shutting down. Foreclosed homes rotting on your block, or being auctioned off on the courthouse steps. The anxiety in the eyes of passers-by. Times are tough.

“Take the unemployment rate,” Williams said. “You ask the average person whether he or she is unemployed, you’ll get an immediate response. They don’t have to think about it. Yet if you were to count all the people who consider themselves unemployed, you’d get a higher rate than what the government reports. Because the government has a different definition of employment”

He’s been saying this for years. And for years, officials with the Bureau of Labor Statistics and other federal agencies have scoffed at his claims.

After checking out the kinds of people who swear by his numbers — blogs dedicated to pumping investments in gold and alarmist conservative web sites such as Daily Paul, King World News, and WorldNetDaily — you might be forgiven for assuming that Williams is something of a crank.

Take the anonymous “financial advisor” who runs the “Coming Economic Depression” blog. Right next to ads for ammunition, dried foods, and “depression & survival guides,” the author’s mission statement is riddled with promises that he or she will “help you come to terms as to what is really happening in the financial world.” “BE INFORMED!” the author adds. “PREPARE YOURSELF for the COMING DEPRESSION! BOOKMARK this BLOG for NEWS 7 DAYS A WEEK!” And right below that, you’ll read an interview with John Williams, who urges readers to invest in gold and silver, while the blog’s author claims that soon, the dollar could be worth as much as Zimbabwean currency.

Is Williams a crank? Is he cynically selling flawed economic models to panicky investors? Some of the country’s most prominent economists certainly think so. But perhaps a better question is: after a catastrophe brought on by people who get paid to be the stewards of our economy, how can you tell who to trust? After all, Williams isn’t the only Cassandra out there. Over the last ten years, a small collection of economists, investment analysts, and hedge fund managers were warning that something was dangerously wrong with the economy, only to be openly mocked from the pulpits of CNBC. On subjects from derivatives and subprime loans to Bernie Madoff, experts in suspenders assured us that nothing was wrong.

Nobody’s laughing now, of course. For decades, the American way of life was built on a breathless optimism, a giddy delusion that home prices always rise, credit cards are your friends, and banks perform best when free of cumbersome regulations. It’s been morning in America for thirty years. Now, that morning brings a bad hangover with it.

So perhaps this is John Williams’ time to shine. Ever since the 1980s, he has been on a quiet crusade, claiming that politicians and their bureaucratic lapdogs have systematically hidden how poor we really are. Now we’re reeling from the worst economic crisis in seventy years, one that was brought on by the obfuscations and risk algorithms of the very people who think Williams is crazy. After all, it wasn’t Williams who had to personally apologize for wrecking Wall Street, but Alan Greenspan.

Americans are learning that perhaps they will have to live with less for a long time to come, and that it’s time to face the facts. Williams believes he has a few, and they aren’t pretty.

Williams doesn’t like to talk about himself. Ask him about his politics, for example, and he mumbles something about being a conservative “with a libertarian bent” before changing the subject. Ask him about what he’d invest in, or to get in touch with a typical subscriber to his newsletter, or whether he wanted to be a fireman when he grew up, and he’d rather not say. But ask him about the time George H. W. Bush rigged the gross domestic product numbers in the early 1990s, and he’s got a story for you.

Once upon a time, there was an incumbent president seeking reelection at the tail end of a painful economic downturn. It didn’t matter that he’d just won a war against a Middle Eastern strongman or been in office when the Cold War ended. People were out of work and worried, and when that happens, they go looking for someone to blame.

How, he asked himself, can I convince people that their lives are better than they really are? Maybe it’s time to put some of my guys to work. And so, alleges Williams, a “senior executive in the commerce Department” paid a visit to a “senior official in a computer firm” and pressured him to pump up his computer sales in a report to the Bureau of Economic Analysis. “The computer sales reporting was boosted, the GDP picked up as a result, the recession ended, and George Bush talked about how the economy was great,” he said. “But people thought he had lost touch with reality.”

Williams tells that tale in a delightfully paradoxical monotone, delivering stories of corruption at the highest levels in the style of someone who has read one too many actuarial tables. Although he now lives in the land of Peet’s and medical marijuana, Williams is hardly attuned to his new home; he just moved out here two and a half years ago to be closer to his son and grandchild. Before that, he spent virtually his entire life in suburban New Jersey. His life seemed destined to be entirely prosaic — he never imagined he’d become a celebrity in the world of gold-standard conspiracists.

“I do my best to publish information that is free of political and Wall Street hype, and that information happens to suggest strongly that anyone living in a dollar-denominated world would do well to own some physical gold,” he writes. “I view myself as an economist, not a ‘gold-bug.'”

But as he began his career as a consulting economist, he began to suspect that something was wrong with the math he was working with. A company that manufactured commercial airlines used a model known as revenue passenger miles to sell their product, and at some point, the model it used to calculate them stopped working. The firm called in Williams to figure out what went wrong. As he bore down into the numbers, Williams claims he found the answer: the numbers hinged on the Gross National Product, and the method by which the government and its partners calculated the GNP was faulty. Williams undid the tweak to GNP, and the model started working again — at least until new changes to the GNP “made the underlying data worthless.”

Soon, Williams said, he began to realize that there were a number of problems in how the government measured the economy — and that he wasn’t alone. He conducted surveys of his colleagues in the National Association of Business Economists, and what he found dismayed him. “What I found in my surveys of the quality of government statistics was that most economists realized they were seriously flawed,” he said. “I mean like 70 percent.”

Worse, he claims that the more his colleagues knew what they were doing, the less faith they had in the government’s data. “The first time I did the survey, I had the chief economist for a major retail organization filling it out,” Williams said. “And he said, ‘You know, I think the retail reports are worthless. I just don’t look at it. But they think the money supply is a good one.’ A second economist said ‘Oh, the money supply is horrible.’ What I found is the people who really understood the numbers they were working with thought there were serious problems.”

This hasn’t always been the case, Williams claims; we had a better picture of the economy back in the 1970s, for example. But over time and incrementally, government officials changed the methodology of measuring key economic indicators, painting an ever rosier picture of the economy, which just happened to benefit the incumbent politicians who ran the government. Or as he said in his calm, bland timbre, “Over time there has been a series of methodological shifts in the numbers to tend to create an upside bias in employment and downside in bias in inflation.”

Soon, Williams threw himself into “reverse-engineering” the government’s numbers. And as he dedicated himself to this project, he grew more and more specialized; where once his consulting business boasted Fortune 500 clients, now he publishes a web site, ShadowStats.com, and a newsletter, Shadow Government Statistics, for a few thousand subscribers, mostly individual investors. Although his most dedicated followers hail from the armies of Internet goldbugs, mainstream business papers like Barron‘s still regularly cite his work as well.

And his work — meticulously detailed number-crunching and graphing out raw data examining changes to the method of collecting and assessing the data — all points to one grim conclusion: For decades, the economy has been much weaker than we’ve been led to believe, and the hole we’re in now is deep indeed.

According to Williams, the picture of our national economic health is seriously distorted in three key areas: unemployment, inflation, and gross domestic product. The real numbers today, he argues, look like the 1930s. Although economists didn’t start rigorously measuring numbers like unemployment until 1940, the best estimate of nonfarm unemployment during the Depression puts the peak at 34 percent. “We’re not there at this point,” Williams said. “But we’re as bad as we’ve been post-World War II.” But you wouldn’t know that, he adds, from the official statistics.

Take unemployment, for example. According to Williams, the government has built a number of minor distortions into how the idle workforce is measured. The payroll survey, for example, depends on the sporadic self-reporting of large companies, and when Bureau of Labor Statistics beancounters realized that small businesses weren’t being adequately taken into account, they just added another 100,000 jobs per month to correct for this.

But it’s when the feds report the results of the payroll survey, Williams claims, that the major distortions show up. The number that gets all the headlines, the so-called U-3 Measure, is the number of utterly unemployed people. A broader measure of unemployment, which is called the U-6 Measure and includes part-time workers and “discouraged workers,” or people who have recently stopped looking for work, usually puts unemployment at a little less than twice what we usually read about.

But Williams claims that even the broader measure is erroneous because sixteen years ago, the feds changed the definition of so-called discouraged workers. “Up through 1994, this was the definition of discouraged workers: You met all the other qualifications, but you haven’t looked for work in the last four weeks,” Williams said. “In ’94, they changed the definition so that in order to be discouraged, you had to have not looked for work in the last four weeks, but you had to have worked in the last year. The result knocked several million people out of consideration. … Those who hadn’t looked for work in the last year just weren’t counted.” The result, he said, is an army of unemployed workers that the government simply redefined out of existence.

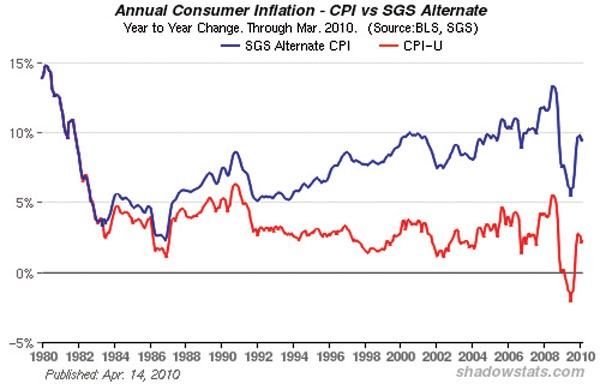

Williams’ most controversial critique concerns inflation, expressed as the Consumer Price Index. The CPI is an index of commodities you need to buy in order to live the average American life: a gallon of gas, a slab of steak, etc. Once upon a time, measuring CPI was simple; you took the price from the year before of all the goods in the index, compared it to the price today, et voila. But in the 1980s, Alan Greenspan and others tweaked the model, adding an assumption known as “product substitution,” i.e., that consumers would switch to cheaper but essentially equivalent goods if the price of any given commodity got too high.

“They said that if the price of steak went up too much, people would buy hamburger, and the cost of living would go down instead of up,” Williams said. “But the CPI is designed to measure what you need to maintain a constant standard of living. It moved the measurement of CPI away from measuring a constant standard of living to something less than that.” And Williams imputes a rather sinister motive behind the change: if you lower inflation with gimmicks, you can reduce everything from interest payments on the national debt to cost of living adjustment to Social Security payments. Suddenly, national leaders had a more transparent interest in arcane CPI minutiae.

This wasn’t the only technical change to the CPI. Geometric weighting assumed that as prices of goods spike, consumers simply stop buying those goods as much, so the goods were given less importance in the index. The so-called hedonic adjustment assumes that as the quality of goods improves (computers get faster, etc.), the overall price in such goods effectively declines as well. Williams scoffs outright at this particular bit of gymnastics, arguing that economists have warped an apples-to-apples comparison with intangibles like “quality.” He notes that for a time, this tweak even extended to MTBE gasoline additives, tamping down the rise in inflation with the notion that improved air quality could be expressed in terms of price. The net effect of this, he claims, is that the government’s measure of inflation has steadily departed from reality. Here’s how it’s changed over time, according to Williams’ numbers.

Williams’ critique of how the Gross Domestic Product is measure is closely related to inflation. The GDP is defined as the value of all goods and services produced in any given period, less the rise in prices. But if the inflation rate is artificially lowered, then the GDP is artificially raised. “If you use a high rate of inflation, that will reduce the growth,” Williams said. “If you use too low a rate, that will increase the growth. And to the extent that the CPI is overstated, there’s a parallel there. I figure that economic growth is overstated by about 3 percent.”

Here, over time, is the government’s estimate of Gross Domestic Product, compared with Williams’ estimate.

If you disregard what Williams regards as official distortions and look at the economy with cold eyes, these numbers are utterly dismaying. They’re an aggregation of catastrophe, an economy that has gone simply catatonic. Williams stares this straight in the face and doesn’t flinch.

“People can’t make ends meet, and they have to cut back,” he said. “And so you’re not going to see positive economic growth until the incomes are growing relative to prices or people go into debt some more. And neither of those things will happen soon. We’re in for a protracted downturn here. We can see down into the valley, and it’s an absolute disaster.”

Of course, he’s been saying this for quite some time. In 1989, for example, Williams said the stock market would take a nosedive, but the Dow Jones closed out the year with almost twice the value he predicted. And frankly, most economists regard his ideas with utter contempt, when they take the time to address them at all. Almost none of the UC Berkeley economics faculty approached for this story bothered to respond, and many who did, like Martha Olney, warned against naive reporters “writing this up as some big conspiracy.”

“There’s certainly no conspiracy among economists to suppress the true information,” added UC Berkeley economist Alan Auerbach. “I’ve never heard of a criticism that the CPI understates inflation. Virtually everyone who criticizes it criticizes it for overstating inflation.”

Far from being a subterfuge to cook the books, Auerbach said, changes to how the CPI is measured actually reflect a more supple understanding of consumer behavior. Take the hedonic adjustment, for example. “When new goods become available, it’s in a sense like lowering prices, because we can buy goods we couldn’t before,” Auerbach said. “As far as product substitution goes, well, that’s what people do. Take margarine. You can shift to margarine without changing your budget at all. … Or suppose that I’m pretty indifferent to buying two different cuts of meat. Now the first cut of meat goes up by a lot. How much has my purchasing power gone down? Not very much.”

Maurine Haver is the chair of the statistics committee for the National Association for Business Economics, and she regards people like Williams as a plague upon her profession. “I realize that there are certain people who just won’t talk to you because they hear John Williams, and they just say forget it,” she said. “But I think it’s important to take the time to explain this, because otherwise there’s no one to speak up against it. … I’ve read a few pieces that I think came from him, that I found rather infuriating and uninformed. Everyone is welcome to their point of view; that’s what’s wonderful about this country.”

For example, Haver has little regard for Williams’ argument about discouraged workers. “If someone has done absolutely nothing in one year’s time, I frankly think they’re not very serious about working,” she said. “The U-6 gives you a measure of the very worst in unemployment, period. I don’t think there are any more people who truly are out of a job beyond that, people who won’t get their butt out of bed. If you have done nothing in a year, do you really think that person is a member of the labor force?”

But it’s Williams’ critique of inflation that really gets Haver’s blood going. Tweaking how we measure inflation is hardly a recent move; economists have been rejiggering price models since they started the project in 1919. Hedonic adjustment, for example, is designed to reflect that fact that as technology improves, you get a better computer — a more valuable computer — for the same price as the previous version. Without hedonic adjustment, the CPI would still measure what it would cost to buy a first-generation Macintosh — but that would be next to useless, since Apple doesn’t sell them and no one buys them anymore. Without it, she said, “We would have buggy whips and slide rules and all sorts of things in the CPI,” she said. “Products come and go, and what you’re trying to do with the CPI is measure the cost of living for an American urban consumer. I don’t know about you, but I don’t have any buggy whips in my market basket.”

In fact, Haver argues that Williams’ most effective argument — that government economists are distorting truths that we all know in our gut — is what exasperates her the most. Take inflation again. How is it, Williams asks, that inflation can be reported in the press at 2 or 3 percent year after year when housing and gas have both shot through the roof in recent years? It doesn’t seem to make sense.

Haver responds that it’s because you’re not really looking at the real price of housing, for example. Yes, the retail price of a house zoomed upward in the last few years. But how many people actually bought a house in any given year? Not that many. Instead, most people either rented or paid a mortgage. Back in the 1980s, economists changed the price to reflect this reality, casting the price of shelter as what you could reasonably charge if you decided to move out of your house and rent it to someone else. And that rate, Haver claims, has remained fairly steady.

As for gas, that is included in the Consumer Price Index. But there’s more than one CPI — the core and the overall index. If you look at the overall CPI, expenses such as food and energy are included, and by that measure inflation spiked to 5.5 percent as recently as 2008. But most of the time, the press reports the core CPI, because the feds use the core to determine monetary policy. And the core CPI is designed to measure the underlying structure of prices. Because a freeze in Florida could suddenly drive up the price of citrus or a refinery explosion could spike gas prices, they’re considered too volatile to be an accurate gauge of what’s happening to prices overall.

Williams doesn’t buy any of that. In fact, he considers core inflation just another “nonsensical concept” that distorts reality once again. “While such information might be interesting over a short period of time when food and energy prices are particularly vulnerable in a given month, over the period of a year, food and energy prices cannot be ignored as part of meaningful consumer inflation,” he wrote in an e-mail. “Even Fed Chairman Bernanke eats food and consumes energy.”

His attitude toward hedonic adjustment is similarly withering: “If a computer now plays movies, then that should be handled as a new type of product and introduced as such. … Instead, the government deems that a computer now is, say, 20 percent less expensive than it was before from a quality standpoint … even though the retail sales price of the machine has not changed. … I should be able to buy the same computer I did ten years ago for $100. To buy the same basics I need, to do the same work as I still do on the old machine, it still costs me $1,000 today. While some adjustments are proper, there are imbalances here that have been taken to extremes.”

Such arguments leave Haver gritting her teeth as she struggles to find a constructive characterization of Williams. “On the Internet, there are people who want to believe the worst,” she said. “And that’s unfortunate. It’s important that we have information about the economy that we can trust. And in Washington, we have all these nerds who are trained so hard to do their best to produce measures that really are accurate in terms of giving us a picture of what’s going on in their country.

But not everyone is eager to dismiss Williams as a crank or a huckster. Kevin Phillips, for example, cited and endorsed his work in a particularly dire May 2008 Harpers piece. “Undermeasurement of inflation, in particular, hangs over our head like a guillotine,” he wrote. “Our humbugged nation may truly regret losing sight of history, risk, and common sense.”

Perhaps you may have heard of Phillips, a former NPR commentator. He’s the author of The Emerging Republican Majority, the 1969 book that predicted that as Americans move from the industrial Northeast to Sun Belt suburbs, a massive ideological realignment would place conservatives in power for at least a generation. He is, in other words, the author of one of the most famous and deadly accurate predictions in American political science. His 2008 book, Bad Money, argued that a convergence of peak oil and unprecedented personal and mortgage debt was about to plunge the nation into a chasm.

If anything, Phillips was already late to that game. All throughout the middle of the last decade, a small number of analysts and hedge fund managers warned that the American economy was crippled with debt, that the housing market was going to tank, and we were all headed for a deep recession, only to be universally dismissed as nuts, “permabears,” and professional pessimists.

One of this era’s defining moments occurred on August 28, 2006, when stock broker and UC Berkeley alumnus Peter Schiff appeared on CNBC and proclaimed that by 2008, our addiction to debt-financed consumption and the collapse of the housing bubble would plunge the country into one of the deepest recessions it had ever seen. Squaring off against Schiff was none other than Art Laffer, former economic advisor to Ronald Reagan and the godfather of supply-side economics. “The United States economy had never been in better shape,” assured Laffer, who even went so far as to bet Schiff a penny that the economy wouldn’t crash. “I’ll be you a lot more than a penny,” Schiff retorted.

Perhaps the most prominent of these Jeremiahs was NYU economics professor and consultant Nouriel Roubini, who traveled around the country in 2006, warning of the coming collapse, only to be dubbed “Dr. Doom” by his condescending colleagues.

Even today, Roubini believes our pain is just beginning. According to Prajakta Bhide, a research analyst at his firm Roubini Global Economics, growth will stay flat at best for at least another year and we face a 20 percent chance of sliding into a second recession. “The growth numbers in 2009, how much of it is from private demand?” she said. “If you look at what is driving the numbers, the underlying fundamentals seem to be a lot weaker.”

At first, the economy seems to be picking up, Bhide argues. Replenishing inventories gave the fourth quarter of 2009 a nice little boost, and the Census drive and a slight uptick in manufacturing will help with employment, but only a little, and only for the first six months of this year. But consumer spending is stuck at 1.7 percent, and consumption comprises 70 percent of the nation’s economy. Meanwhile, the housing sector is a disaster; housing starts are still declining, and Bhide predicts that nationwide, real estate prices will still have to fall another 3 to 5 percent before they bottom out.

In fact, Bhide argues, unemployment will keep the American economy crippled for at least a year, if not more. “You will see job creation, but it won’t be enough to stop unemployment from rising,” she said. “The economy needs about 250,000 additional payroll jobs each month just to keep the unemployment rate from rising further. We’ll see some rise in payroll jobs in the first half of 2010, but it won’t be enough. And we’ll see unemployment rise till it peaks in Q1 of 2011, most likely.”

Now, of course, Roubini and Schiff look like geniuses, or at least right. But for years, the smartest guys in the room rolled their eyes and chuckled at the mention of them. In hindsight, our boundless American optimism clearly got us into this mess, as we told ourselves we could always amortize the consequences of our overconsumption, spending, and debt. But so did our experts. The men and women who we trusted to know better, who dazzled us with their jargon and numbers, harvested billions while the world crumbled.

For years, fund manager Harry Markopoulos warned the Securities and Exchange Commission that Bernie Madoff was running the largest Ponzi scheme in history, but it turns out that SEC managers were too busy visiting pornographic web sites to care. Goldman Sachs, the only big-ticket money firm to weather the crash, now stands accused of widespread fraud. That old Ayn Rander Alan Greenspan even had to slink into Congress and admit that he had “found a flaw” in the ideology he imposed upon the American economy.

If John Williams is wrong, as so many experts tell us, it’s a measure of how profoundly our most important institutions have failed us that he doesn’t seem that wrong right now. How likely is it that Williams, almost alone among the entire economics profession, knows the truth? Then again, how likely was it that that Wall Street, the federal government, and the credit rating agencies knew less about the mortgage bond market than a one-eyed, Asberger’s obsessive, sitting in his San Jose living room and shorting subprime securities, the story of which is told in the compelling book The Big Short by Michael Lewis?

Everywhere you look in America, you can see the erosion of public confidence in our foundational institutions. The media took its hit long ago, of course. But scientists are now widely derided as cooking climate numbers. Congress now has the lowest approval numbers in history. Bankers, once the dullest and most dependable citizens of the republic, are hiding in the Hamptons until the rage dies down.

No lay person can judge the merits of John Williams’ arguments; we just don’t have the expertise. We used to find the people who were trained to know better and ask them. But in this climate and at this moment, that may not work for the public anymore.

Even Alan Auerbach, the Cal economist who thinks so little of Williams’ work, acknowledges that the public isn’t in the mood to listen to guys such as himself. “I understand that it’s hard,” Auerbach said. “It’s hard for economists to say don’t listen to this guy. Because we’re not always right. Just look at the crash. Anything can happen.”